news The Commonwealth Bank of Australia this morning revealed several devices and an application development platform that together constitute an ecosystem similar to the Square mobile payments system which is becoming popular in the US for transactions at merchants such as retailers, restaurants and cafes.

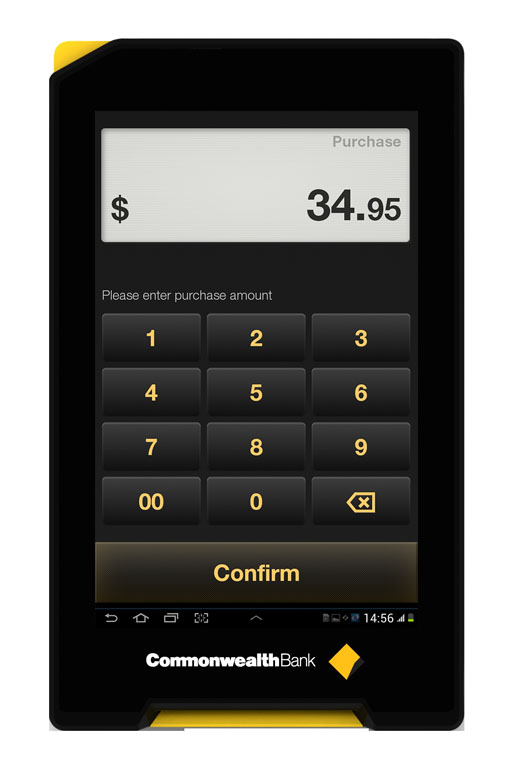

According to a media release issued by the bank this morning, there are several pieces to the puzzle, which it hopes will “revolutionise” the point of sale experience for Australian consumers. The first and most obvious piece is Albert (pictured above), a new mobile payments terminal which uses an underlying platform based on Google’s Android operating system. The device features a 7″ touchscreen, a PIN keypad interface, a paper printer and merchant terminal functionality similar to today’s existing EFTPOS terminals.

Secondly, CommBank has also developed another hardware system which it calls Leo. Leo attaches to Apple iPod Touch, iPhone 4 and iPhone 4S devices to transform them into “a fully functioning merchant terminal”. It is this functionality which Square is famous for providing in the US. CommBank has previously used Ingenico hardware for its Kaching! consumer mobile payments solution, which adds an NFC chip to the same Apple smartphones through a surrounding case.

CommBank also this morning unveiled a software platform which it said would run on the Albert, dubbed ‘Pi’, as well as an application ecosystem, AppBank. The bank said that applications could easily be created for use by merchants on their Albert or Leo systems and distributed through AppBank. The Pi and Albert platforms were developed with the assistance of banking technology vendor Wincor Nixdor and design house IDEO. You can watch a video demonstrating the whole lot here.

“Pi, together with Albert, will empower businesses to go beyond a simple transaction by using consumer-friendly applications and a human-centric interface to enrich the customer experience,” said Kelly Bayer Rosmarin, Executive General Manager of Corporate Banking Solutions, Commonwealth Bank. “From offering an easier way of splitting the bill, activating a loyalty program, using information on customer preferences, to offering a more personalised experience or checking stock – with Pi, the opportunities are limitless.”

“We know businesses want to have richer relationships with their customers but have felt restricted in the ways they can do so. Pi will help break down these barriers, having been designed from the ground-up and based on actual business feedback to deliver a solution that will revolutionise the customer experience. Interactions between businesses and their customers will never be the same again,” the executive added.

“CommBank is committed to providing game-changing, human-centric innovations for our customers and we believe Pi firmly delivers on this commitment. We look forward to continuing to work with our business partners and welcoming new developers on board as we work towards general availability and rollout of Albert in 2013.”

Albert will commence its certification this year, with expected general availability, depending on the time taken for final certification, in the second quarter of 2013. Leo is currently being piloted and will be available to other businesses in August. Apps developed for CommBank’s platform will be subject to approval by the bank, with Pi being available immediately for developers to begin working with.

One example of an application given by CommBank was the ability to split bills at a restaurant through the Albert platform.

The main rivals for CommBank’s new ecosystem are likely to be the existing EFTPOS system, which is ubiquitous throughout Australia but limited in its application, and Square, which announced in June that its technology had been adopted by over two million individuals and businesses throughout the US. However, Square has not yet launched in Australia, as it has remained focused on its home market of the US.

Square’s Card Reader plugs into the headphone jack of an iPhone, iPad, or Android device and allows for credit card payments through the free, downloadable Square Card Reader and Square Register apps. Square charges a rate of 2.75% per swipe, and Square merchants have access to their funds the next business day.

opinion/analysis

Wow. Suddenly CommBank has an Android-based intelligent EFTPOS-style terminal. Suddenly it has hardware devices which plug into an Apple device, just like Square. Suddenly, it has a whole operating system and app ecosystem which it wants third-party developers to tap into. Maybe CommBank is actually serious about its future competitors being Apple and Google.

So what do we make of all of this? After thinking about it for a while, I want to make three points about what the bank announced today.

Firstly and most obviously, this whole initiative by CommBank is a colossal attempt to lock in retail merchants all around Australia to using its banking platform for the foreseeable future. The bank didn’t say as much this morning, but I’m betting you won’t be able to use Albert, Leo, Pi or anything else unless you’re a CommBank banking customer. You won’t be able to take this platform with you if you become a customer of ANZ Bank, for example.

However, as most of Australia’s retail merchants are already locked into this kind of deal — with existing bank-branded EFTPOS terminals, they likely won’t see this as a big deal. Most will see it as CommBank upgrading its existing fleet, rather than a radical new revolutionary move etc.

Secondly, I predict the bank’s attempt to get third-party software developers interested in developing their own apps for Pi will broadly fail. CommBank is not a major software vendor like Microsoft, and it has no experience in working with third-party software developers. Those who do choose to work with the bank will likely find it to be inflexible, overly bureaucratic and a stickler for the rules. Every bank is.

As for the initiative as a whole … I think that it’s too early to call whether it will fail or not. In the US, Square has pioneered great change in mobile payments for retailers, and the CommBank is clearly attempting to steal a march on this invader by copying its model and launching in Australia before Square or someone else can.

But Square’s own future — and the future of the whole mobile payments industry — is very much up in the air right now. In the mix are the other banks, the EFTPOS organisation, the credit card companies VISA and Mastercard, the regulators such as APRA and even companies like Apple and Google. I don’t know whether anyone really wants CommBank to be disrupting this ecosystem, apart from CommBank itself. Certainly I haven’t seen any real demand for the “revolutionary” new products it launched this morning.

Right now, CommBank is doing the right thing in attempting to innovate in Australia’s banking system, especially when it comes to payments. However, to me all of the bank’s initiatives have so far felt very much like the sorts of product launches we’ve seen from book publishers, newspapers and record labels over the past few years.

All of these organisations tried hard to build new technology models to shift their business into a new digital environment, and all of them broadly failed. And they failed because they are not technology companies and they don’t understand technology. It took actual technology companies — Apple, Google, Amazon — to succeed in evolving their models.

I think the same will eventually prove true of banking. Despite the Commonwealth Bank’s best efforts, I suspect that nobody really wants their bank to be a technology vendor. But in a few years’ time, what we may find is that a few technology vendors may do a better job of providing for our future banking needs than the banks ever could.

Image credit: Commonwealth Bank of Australia

The only way I could see third-parties working on this is if most of the local banks agree to a common set of standards, with individual banks then approving apps into their own appstore.

Aka Android + PCI DSS requirements and whatever else. Bit like how things are with Amazon and Google.

But I think we will see pigs fly first.

+1 to the pigs flying bit.

PayPal is already offering a card reader for iPhones. It’s called PayPal Here and unlike Square is available now to Australian merchants.

True — I had forgotten about that. However, I have to ask — who the hell would want to form a serious business relationship with PayPal? They’re one of the most awful companies to deal with that I know.

PayPal’s OK. They have to be strict because they’re dealing with financial transactions. Using their APIs takes work, but once they’re mastered, they are rock solid.

PayPal is what the banks are scared of.

I dunno. When there’s nobody to call, they don’t respond to emails, and their automated system re-requests 3 times in a row that you fix your company letterhead to meet their standards or else they won’t approve you for a business account, PayPal is what I’m scared of. In my pantheon of soul-less, inhuman corporations, PayPal is on the top of the list.

I am basically forced to use PayPal online, but I personally hate, fear and loathe the company.

Paypal scares me too. There are parts of how they do things that make me think they are a less transparent version of Apple – you vill do vhat vey say or else NO PAYPAL FOR YOU!

Somehow along the way they have become THE standard for online transactions though, and thats a LOT of bargaining chips they have to play with. Like Apple with a few of their products, they have the high ground simply on volume, so have the luxury of dictating how things are going to work. Dont like it, whats the practical alternative. And they seem to be abusing that position.

THATS what worries me.

I don’t know about Australia, but in the USA PayPal is not classified as a bank. Not someone I would want to trust with my money.

http://en.wikipedia.org/wiki/PayPal#Bank_status

Bold of CBA, and good luck to them. I agree with the sentiment they want to be ‘in there’ before someone else steals their thunder. Look at iTunes – the reality is a tech co. is a music reseller.

But sometimes I can’t help be cynical and think that collectively banks tend to forget that average joe public just wants to get on with business, and that their technology is actually a problem, not a solution to doing business.

everything, it seems, these days is touchscreen even these new eftpos terminals.

will the new ATMs they’re rolling out be touchscreen too?

I suppose the real issue is: how affordable will this be? From what I understand of Square, even if I wanted to set up a tiny, test business – say, selling prints of my photos for $5 at a market stall – their product would let me take electronic payments with no up-front charge. I doubt that the Commonwealth Bank would be as disruptive.

My gut feeling is bleak. The last people who want to turn business models on their heads are the major banks. I hope Square comes to Australia soon.

Impressed with Commbank keeping up with tech, first Kaching and now mobile payments.

I’d rather deal with Commonwealth than Paypal. If they move quickly they could gain a foothold in the Australian market before Square et. al. expand here.

Paypal Here is really easy to use and will be launched Australia wide soon. I haven’t had any problems contacting them by phone or email for enquiries. I don’t know why people are scared of Paypal.

Modern banks really are technology companies; it looks like CBA is one of the first in Australia to realise it, and that it’s about time they acted like it.

What is a bank nowadays? It’s a few branches and customer service staff as the “soft” interface layer between the man on the street and a massive datacentre.

What advantage does PayPal offer to the average Joe in Australia?

As a consumer, unless you’re an eBay junkie or do lots of small, personal international remittances, there is no benefit over EFTPOS/Credit Cards at the POS and intangible benefits for using other features – most banks have fee free accounts and low fee credit cards so you’re effectively covered for domestic (DE) payments (P2P) and online, as well as having smartphone app and internet banking access.

For the merchant? According to PayPal’s website for < $5,000 sales, it’s 2.4% + $0.30 AUD, which is about what most traditional bank merchants will pay, so where’s the benefit?

I’ve seen plenty of PayPal presentations and each time I’ve never been able to see the advantages, and always think to myself “my bank can do that now”.

Damn I was under the impression I could get Square here in Australia. I have just ditched my Commbank eftpos. I am an artist with a small gallery but mosty wholesale business and once you add monthly service fees, terminal rental fees and the percentage for each transaction its money I can not afford except in the spending season which is Christmas. Most of my customers pay via direct debit but I do need a retail credit facility. I was about to go buy an Ipad as point of sale and get Square…or so I thought….

Banks are like airlines. They are regulated fairly strictly but essentially all do the exactly same thing so the only differentiator is their “brand”.

The experiences I have had with both industries is that the “brand” holy grail and their obsessiveness with it is often to the detriment of their own business and almost always to the detriment of their customers.

Still waiting on CommBank to come out with this..

I am guessing i will be waiting a while..

Comments are closed.