news National broadband provider Internode has changed its business broadband bundled plans to be identical to those of parent iiNet, in the latest sign that the Adelaide-based ISP will follow other iiNet acquisitions Netspace, Westnet, AAPT and OzEmail and become just another brand under the larger iiNet group.

When iiNet announced it would buy Internode in late December 2011, the two companies were careful to highlight their plans for the South Australian ISP led by well-known industry figure Simon Hackett to remain independent from its new parent. “This is another iiNet acquisition and Internode will just disappear, right?” stated a question posted as part of Internode’s frequently asked questions document for the transaction. “No, it isn’t,” came the answer from Hackett. “Internode will be remaining as a separate operating company within the group, with its own identity and its own staff. I am staying at the helm of Internode as is the rest of the management structure of the Internode & Agile company group.”

At the time, Hackett emphasised that his new status as a major shareholder of iiNet itself would mean that Internode would not “just disappear into iiNet without trace”, and that there was little reason for the company to harmonise its broadband plans and offerings with those of iiNet, as other companies subsumed into iiNet — such as Netspace, Westnet and AAPT — had in the past.

Since that time, Internode has maintained its existing broadband plan structure, with its business and consumer plans remaining differentiated from those of iiNet, unlike iiNet’s other ISP brands, which have harmonised their offerings with those of their parent. However, in a statement issued by Internode this morning, the company flagged plans to overhaul its broadband plan structure for businesses.

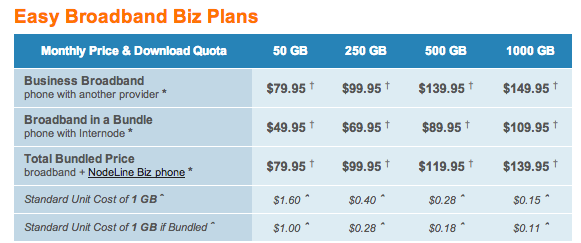

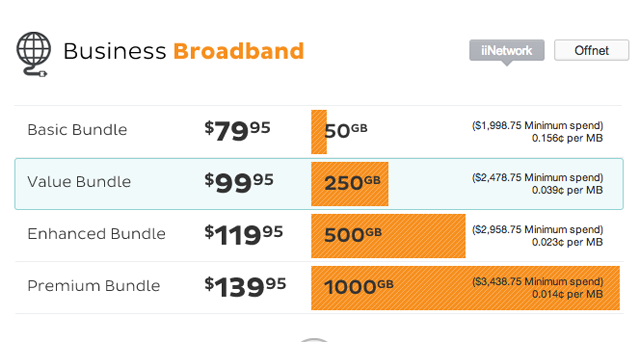

The media release didn’t mention it, but Internode’s new business bundles are precise replicas of iiNet’s existing business bundles. Both brands offer four bundles at $79.95, $99.95, $119.95 and $139.95 price points, and offering 50GB, 250GB, 500GB and 1000GB of quota. Each comes with a bundled telephone line offering included local and national calls. The new Internode plans also come with a precisely matched list of other features also listed by iiNet, such as 20 included email mailboxes, static IP addresses, priority business customer support and so on. Internode’s non-bundled plans also appear to have been harmonised with iiNet.

In its release, Internode product manager Phil Dempster pitched the new offering as delivering greater value. “These are perfect for businesses that want to get more bang for their buck from their communications spend,” the executive said. “As phone calls are a big cost to any business, our NodeLine Biz service provides great value by including local and national phone calls plus offering attractive call rates to mobiles and overseas.” The consumer offerings of the two brands still remain distinct from each other.

Over the year and a half since the acquisition, iiNet and Internode have increasingly tied their operations together. Internode’s chief technology officer John Lindsay, for example, migrated last year to the equivalent post at iiNet.

The news came after iiNet also announced the merger of the 3FL and games.on.net Internet gaming platforms which had separately been operated by iiNet and Internode respectively. The new merged platform was combine “the best features” of both and will retain the games.on.net brand name, according to an iiNet media release issued at the time. “By combining iiNet and Internode resources and staff, we can offer the latest news, reviews and interviews plus more than eight terabytes of files, trailers, mods and patches and a 10,000 player capacity,” iiNet chief product officer Stephen Harley said.

iiNet and Internode have also integrated a number of other areas of their businesses since the acquisition was finalised last year.

In March last year iiNet introduced Internode’s data blocks feature to its own broadband plan structure, and then several weeks later iiNet also dumped the on-peak/off-peak split of its broadband plans, offering customers the same base system as Internode has long promoted for its own plans. Both moves came after Internode announced its intention in February last year to migrate customers using wholesale offerings from rival companies like Optus and Telstra to iiNet’s ADSL infrastructure where possible. With similar moves occurring on iiNet’s end, the move effectively integrated the ADSL infrastructure owned by the two broadband companies.

opinion/analysis

I have known for a long time that iiNet would not be able to resist harmonising the product offerings of Internode with its own, and it looks like that integration is about to kick off. No doubt it has only taken iiNet this long because of the highly independent and successful nature of Internode as an independent business. But I don’t think anyone on a broadband plan at Internode should be under any illusions — Internode is definitely part of the iiBorg collective now, and will no doubt be fully assimilated shortly. Resistance is futile. Ah, competition in Australia’s broadband sector. We barely knew ye.

Image credit: Paramount (From Star Trek)

Silly ACCC with their 121 points of Interconnect “reasonable middleground”.

Bet they’re eatting their words now. Or maybe they too have been assimilated.

Resistance is futitle.

Heh. The sky is falling ! The sky is falling!

(Actually, is isn’t).

Nice observation, Renai – and accurate at face value – that the new business plans are the same as the iiNet ones.

… but hardly surprising at this point, some years after the comments you quoted in this article were made.

The iiNet customer base traffic is carried, these days, on the (suitably expanded) Internode national/international network, and as a result, the underlying cost base for moving traffic is essentially the same across the group. We’d have been mad not to do that, and I’m really proud of the extent to which the Internode network is the backbone of much of the combined group traffic carriage these days.

This meant that as we looked to updating Internode business plans, there just wasn’t any rational reason *not* to align the business plan pricing in this specific change, because these plans are in turn a product of the underlying economics of carriage. Surely that is no surprise to anyone. Creating or maintaining artificial distinction just for the sake of it doesn’t seem sensible, past some point – and in the business plans, we simply reached that point.

Neither does it seem sensible not to have merged the underlying carriage paths concerned, because not doing so would have raised operating costs for us in an industry in which *failing* to optimise underlying economies of scale would be pretty insane.

Residential broadband plans remain different for various reasons (including some differences in network deployment mechanism that remain in place between the Internode and iiNet customer bases in terms of the way that residential network data sessions are terminated and managed by Internode vs iiNet.

It won’t be a ‘sky is falling’ day, either, if (in the future) the residential plans wind up being harmonised at some future point. Again, there will logically be a future point at which there isn’t any merit in maintaining what may have (by then) become an artificial/historical distinction, and in a world in which quotas just keep tending upward (and hence in which the sensitivity to the nuances of specific broadband plans tend to trend toward being less critical for customers as well).

The sky might have been closer to falling if, for instance, Internode had driven in a peak/offpeak quota system (instead, iiNet removed theirs in favour of the Internode approach). Or if Internode had stopped selling data blocks (instead, iiNet started to offer them as well!). Hey, is your thesis really that Internode is disappearing into iiNet, or that iiNet is disappearing into Internode? :)

But: Two points about the previous paragraph are worth noting here:

1) FWIW, The residential plans are not actually slated for harmonisation right now

(Of course, this is not a ‘for all time’ prediction, just as what I said in 2011 didn’t come with a rider of “and I promise Renai that nothing I just said will ever change for any reason, years from now”)

2) The only comments our customers tend to make in comparing iiNet vs Internode plans these days is in the context of wishing they -were- the same because that’d lead to a simpler life and to the avoidance of scenarios of having to change providers just to get access to some thing that one sells and the other doesn’t. The only logical end point is that both brands offer the full suite of outcomes generated across the whole group.

Its also worth appreciating that all existing customer plans remain grandfathered as is our usual practice, so the consequence of the presence of the revised business plans on existing customers is that they are at liberty to change or not to change – and aren’t being required to change if they don’t feel like it.

Here’s the thing:

These gradual harmonisation in terms of what you can buy and what the plan looks like don’t intrinsically correspond to the imminent disappearance of Internode as an entity in the environment. That would only make sense if you believed that the entire identity of Internode is defined by the specific plans on sale at any given time – and that just ain’t so (and it never was).

The plans we run (and any future changes in plan that may occur) are going to be a highly logical consequence of technical integration of the underlying national and international networks. That integration is as obvious as it is sensible – because one of the whole points of the merging of Internode into the iiNet group was to gain the benefits of economies of scale in terms of the future of both companies.

So its logical that Internode and iiNet plans and services will continue to cross pollinate – with each gaining benefits from having access to the efforts of the other. In the long term that naturally tends toward the underlying plan constructs becoming harmonised (see above), unless there is some benefit in artificially keeping them different that you can see and that I can’t.

And that -still- doesn’t mean the sky is falling :)

Anyway – its the bow that you’re drawing here (must be a slow news week), from ‘plans becoming more harmonised across the group’ to ‘Internode disappearing without trace’ is really the piece I need to gently take issue with.

For instance: iiNet are starting to offer the SHDSL based business tail circuits that Internode has built around the country. Does that mean that iiNet is going to disappear inside of Internode? Well, of course not – but likewise the reverse is an equally incorrect conclusion to draw.

The Internode brand, its staff, and its contribution to the industry haven’t all magically evaporated just because you’ve posted some Star Trek images here, mate. Or because we’ve done sensible things in terms of ensuring that we use the resources of the group in a collectively sensible manner for the benefit of all of our group customers.

The Internode brand is a strong one, it holds a customer satisfaction rate and a position in the industry that remains distinct to iiNet (and indeed remains the only industry brand that surveys externally to a higher level of customer satisfaction than the iiNet brand :) ).

As a result, I must say that your prediction of the imminent end of the Internode brand is at odds with observed reality, and also at odds with the increasing amount of advertising we’re doing under the Internode brand these days :)

You ought to turn up at a few more industry events again mate – I miss seeing you at my continuing appearances at CommsDay and similar events to talk about the industry. My next one is in July in Sydney at the Commsday wholesale and data centre event. I hope your busy schedule allows you to get out more in the coming months and then we could have more of a chat about the future of the industry in person again.

Or maybe take a holiday to SA next year to enjoy another fine Internode sponsored arts event like Womadelaide or the Adelaide Fringe and I’ll buy you a beer while you check your email using an Internode hotspot.

Best wishes,

Simon Hackett

Admit it Simon, you’d get bored with the media if I ever retired ;)

Absolutely so, Renai.

oops, forgot to add:

“:)”

that’s all very well and good, simon, but as a long time internode customer (over 7 years), i am willing to bet my house that in 2 years time, internode, as it stands now (or before) will cease to exist.

we’ve seen it before with other brands that iinet purchased. i fail to see how it won’t happen to internode.

but hey, it’s a free market economy.

little comfort to those who made internode what it is today: it’s customers.

I understand IINET model is pretty much Hotelling of spacial competition. If you don’t know what that is check this ted talk

http://www.youtube.com/watch?v=jILgxeNBK_8

You could argue this isnt great for competition because both brands are meant to be separate. Instead the decisions are being made with authority of another company by offering at the same price

The biggest concern for me. Is Internode loosing it identify of being ‘cool prefered geeky isp’ and slowly developing into “another ISP trying to win my attention”. What happened to the first of innovation and feeling of premium service, Pretty much I get more value with IINET atm with freezone

Only the years slowly the ‘cool prefered geeky isp’ focus has been switched to “Mum and Dad”. But then IINET took some ownership in the company and basically two companies are fighting for the same business

However in the case of IINET and Internode. There too much resources sharing or you have Internode staff being trained/recruited by IINET, So employers loose the companies brand identify and work to IINET standards. Not common internode standard perhaps

If only we could get responses like this for even 10% of the articles Renai writes.

“These gradual harmonisation in terms of what you can buy and what the plan looks like don’t intrinsically correspond to the imminent disappearance of Internode as an entity in the environment. That would only make sense if you believed that the entire identity of Internode is defined by the specific plans on sale at any given time – and that just ain’t so (and it never was).”

This more or less sums up my thoughts.

There really is no-one else like Hackett in the industry who can manage to write a comprehensive and (generally) humble answer which patiently and respectfully debunks and explains the issues. Years and years of practice on Whirlpool I suspect. But then, he started off this way, which is why Internode grew so rapidly as the ISP de choix among geeks — an ISP with an engineer-CEO who bothers to take the time to talk honestly to customers. Hats off to him.

This is why I am also a decade-plus customer. Nonny-moose is now on a 50/20 nbnco plan (only just turned on) and while I could have more gigs it’s all the other aspects that keep me, especially Simons …umm iunno, educational postings ? over the years,…and there have been many :)

The only thing I lack is a nodepony. :p

Drop me an email, I will see if I can do something about the NodePony :)

Drop me an email, I will see if I can do something about the NodePony … ‘

I hope you are looking forward to the NBN post a September Coalition win, after all you have a head start with all the free advertising with ‘Fibre to the Node’.

:)

Despite his dislike for some of the decisions, like the POIs, I am under the distinct impression that Mr Hackett much prefers the NBN policy over the Coalitions.

Just call it a gut feeling.

Two articles for the price of one! I’m impressed.

Two articles?

One article… and one press release full of vacuous, tedious corporate-speak.

Some deep thinking there. They really are out to get you, you know.

“one press release full of vacuous, tedious corporate-speak”

Don’t be so rude about Renai’s writing, I happen to quite like it.

Trololololololo …..

Hey ‘deep thinker’ – I can see that some people still enjoy making ‘Ad Hominem’ attacks instead of addressing real issues, but personally – I’m not one of them.

Thats not exactly a good example of ‘deep thought’, now, is it?

He must be really smart. He used words like “vacuous”.

Don’t pay him any attention Simon, he’s a serial troll on here. As someone pointed out a few weeks ago, it’s interesting just how many of the virulent LNP supporting FTTN apologist right-wing trolls have monikers claiming association with a higher power or access to greater knowledge/information/truth/intellect instead of simply being confident in the strength of their argument…

BTW thank you for taking the time to address Renai’s article personally and so thoroughly. This kind of top-down competence has always permeated Internode to its core and is why I used to have so many clients with Internode prior to iiNet’s ADSL2+ deployment over here (I’m in Perth). I personally hope Internode retains its culture and unique identity going forward, but even if that’s not possible I still think Australians will always have access to one of the best ISPs in the world as long as you and Mike Mallone are at the helm of iiNet.

The one thing i would like to know is when it comes to NBN

will iinet and internode buy separate NNI and CVCs

or will iinet (or internode) will only get 1 NNI and CVC

and all AVC be it iinet customers or internode customers go via the one CVC and NNI

?

Maybe i should ask in Whirlpool

Currently there are separate NBN CVCs for iiNet and Internode but the network between the NBN POIs and the service pops is identical.

That is inefficient so it will stop once the automated NBN provisioning systems are running. This will improve performance and reduce costs both of which are good for our customers.

(121 POIs, potentially thousands of CVCs! It’s a nightmare to keep on top of capacity planning because NBNCo require that we order specific amounts and pay $20,000 per gigabit per month for it.)

The global IP peering and transit network will be identical for the whole group in two weeks. The IP core is identical right now. There are differences in the access layer of the network but only to ensure customers get the right experience. We are planning to service most iiNet ADSL customers from lightly loaded boxes that are currently servicing Internode customers which should have no customer impact other than allowing IPv6 to work for iiNet and IPoE to work for Internode.

Internode is a different brand to iiNet with different retail products and that will continue.

But it would be silly to turn Internode into a museum brand, stuck in time.

Onwards and upwards with more and better to come.

jsl

iiNet CTO

Formerly Internode CTO

Formerly iiNet Network Operations Manager

Oh, and formerly iiNet (SA) Operations Manager

‘The Artist formerly known as ‘John’.

“But it would be silly to turn Internode into a museum brand, stuck in time”

Like described in the ted talk I linked earlier.

It seems that both IINET and Internode are competing for the same customers, same space and no differentials space between the companies. Its not good business model and keep spinning the same media positive message “we won’t”

Take for example business case Silvio’s Dial-A-Pizza and Dominos:

Silvio’s Dial-A-Pizza, established by brothers Silvio and Fel Bevacqua. Silvio’s Dial-A-Pizza began Australia’s first home delivery service in 1980. By 1993, Silvio’s had over 70 locations. In 1993, Silvio’s bought the master franchise for the Domino brand in Australia and New Zealand,

In 1993, Silvio’s purchased Domino’s in Australia. The Domino’s and Silvio’s brands were operated separately. Until 2001 when the companies decided close Silvio brand down and operate under the dominoes brand when dominoes board invited both Dom and Andrew, whom at the time were successful owners of a large chain of franchises in QLD to run the company

Understandable when you take the heart and brains out of the company. That company will eventually reach a point where can no longer operate independently even with cleaver marketing and customer servers which only deliver minor differentials to a customer

At the end of the day the customer is either gonna flip a coin or goto closes brand

As discussed previously IINET only wanted Agile network and Internode Business Client was too good a deal to snap up because generated the most revenue. While Adelaide domestic market was just a side salad and extra customers around australia

I am not Flynn will be sending Internode pony will be sent to the glue factory anytime soon. Eventually someone will have to make a decision because will be not a good business model long term to operate two companies

Correction

* I am not saying IINET Flynn will be sending Internode pony to the glue factory anytime soon

http://drawception.com/pub/panels/2012/6-20/mmxXHqEYBX-2.png

So, everyone will (eventually) be on AS4739?

I would hope that they would be sane enough to register a second one for redundancy.

Maybe a better question is “So everyone will eventually be on a IPv6 capable connection?”

After all not everyone here remembers AS numbers off by heart.

Let’s have a look at the list of ASNs that iiNet currently own/control:

4739 – Internode Pty Ltd

4802 – iiNet Limited

4854 – Netspace Online Systems

7498 – Chime Communications

7718 – TransACT Capital Communications Pty Ltd

9543 – Westnet Internet Services

18371 – Neighbourhood Cable

24037 – Fusion Enterprises Pty Ltd

37928 – TransACT Capital Communications Pty Ltd

I’d say AS4740 (OzEmail ISP) is also theirs, despite being dead for a number of years.

So, it would appear they have plenty already. :-)

That is my round-about way of asking “Will everyone be on the Internode network?”

I guess the easiest way to bring IPv6 to iiNet customers is to put them on the Node network (rather than continue development on the iiNet side), but I believe they are moving Node customers to the iiNet billing system as well.

The Internode network doesn’t have enough bandwidth to support all iiNet customers. If they do anything they will merge their network assets, but in all likelihood their implementation will probably result in more than one ASN utilised. Consolidating multiple networks that utilise multiple equipment vendors and route configuration is not a trivial task.

Why don’t you ask what you mean instead of such a cryptic question then?

The NBN Points of Interconnect and the future of competition blog post by Simon Hackett provides some background to the impact of the decision to build 121 POIs and the prediction that competition would be limited to around five players, chiefly due to the cost of CVC.

The fact that iiNet and Internode are now utilising the same infrastructure, means the network performance is likely to be very similar. Both are seen as “premium” RSPs so this isn’t of much concern. Where it becomes more interesting is to consider the case of a premium RSP also run a budget brand (e.g. Qantas & Jetstar).

If we assume that the POI will be the most likely choke point on the network due to the high cost (minimum of $40,000/month for a POI with 2 or more 1Gbps services), it seems likely that both share the same POI connection (as iiNet and Internode will shortly). Premium providers attempt to provide a network without contention, whereas budget providers limit costs by permitting some contention during peak periods (especially providers of unlimited plans). Airlines through bitter experience found that you cannot run a budget airline within a premium airline, because even with shared services, the cost structures of the premium airline make the budget airline uncompetitive. The workable approach is to establish the budget airline as a separate company.

This is model is challenging to implement on the NBN, because the CVC costs are high and sharing does deliver significant savings through load balancing. This leads to one of two potential outcomes:

1) The budget brand delivers performance well above other budget carriers

2) Performance of premium brand suffers because of congestion caused by budget users at the POI.

It would be interesting to speculate on Telstra’s proposal to buy Adam Internet last year and how it would impact on both brands. I suspect Telstra would use Adam to gain customers that wouldn’t pay the “Telstra” premium and those customers would receive good service.

Of more practical interest question of how wholesalers (or network aggregators) will manage impacts of resellers on network performance, and what the means for customers.

When Bigpond controlled the national interconnect. It actually did the opposite of what Simon described in ” NBN Points of Interconnect and the future of competition”, when DSL was launched then wholesaled it created more competition, Only those which carefully made a innovated, were reliable and fast product survived

How they did that. Is they focused on target market or niche industry where they could build up a loyal following and then invested in their products to deliver a more national service

As Conroy keeps saying. The cost will eventually come down over time and so will the backhaul and not going to happen until 2016 when NBN might be cheaper.

Just don’t believe the hype the competition sky is gonna fall.

In the meantime companies have got a 3 year headstart to gain customers

+1

> When Bigpond controlled the national interconnect. It actually did the opposite of what Simon described in ” NBN Points of Interconnect and the future of competition”, when DSL was launched then wholesaled it created more competition, Only those which carefully made a innovated, were reliable and fast product survived

Telstra’s wholesale was a very different scenario. Telstra Wholesale delivered the data to capital cities, whereas NBNCo is 121. The point SImon Hackett made in NBN Points of Interconnect and the future of competition is that this created huge costs for RSPs. As John Lindsay made the point above $40,000 month minimum to support 2 1Gbps customers. NBNCo has acknowledged this reality and as a consequence is currently providing 150Mbps free at each POI. Instead of $40,000 x 14 under the model preferred by RSPs, the cost is $40,000 x 121 = $4.48 million / month just in CVC charges for a national RSP.

You may also remember that prior to Internode launching ADSL2+ services, most plans on Telstra wholesale were very similar and there was little innovation. The variety of options in plans and innovation was started by Internode selling ADSL2+ without speed caps. Internode’s flatrate was an interesting idea that failed because it could not attract sufficient light users. It would be interesting to try these plans under NBNCo, however, NBNCo don’t provide the necessary network configuration to make this possible – a barrier to innovation.

> Just don’t believe the hype the competition sky is gonna fall.

We’ve already seen competition and innovation lessen. The monopoly created by Labor mean that it is unlikely to see significant innovation because of NBNCo’s pricing structure.

Assumptions of this arguement that are false and immediately breakdown arguement:

1) RSPs have to provide 1Gbps services from day one. They don’t, in fact most will probably slowly increase the maximum speed tier rather than offer 1Gbps.

2) In order for RSPs to provide 1Gbps service they must make it avaiable are every PoI. They don’t, they can pick and choose the most profitable areas to get 1Gbps first, thus reducing the impact.

3) The cost of CVC is set at $20/Mbit. It’s not, the price, according the business plan, and basic common sense, is set to drop over time.

What about their network configuration prevents this set-up? You can’t just say it, and expect us to believe you. Based upon your track record, including the easily demonstrable counter points I presented above, I don’t trust you to actually understand anything about the NBNCo pricing model and how it afters RSPs.

I don’t know if you know this but Flatrate plans were suggested by Exetel under the NBN after-all. Whether or not this was just a positing of a “better way to do thing” or something that Linton actually plans to implement remains to be seen, but there was no press release as far as I’m aware of saying “NBNCo’s pricing model stops us from offering this product, sorry.”

Honestly, although consolidation by companies like the iiBorg occurs in part by NBNCo, you cannot assume that the existence of NBNCo is the only reason for this. In fact, I’d say that the iiBorg would have made a considerable number of acquisitions even without the NBN, simply because they could. Correlation does not imply causation Mathew.

Honestly, although consolidation by companies like the iiBorg occurs in part by NBNCo, you cannot assume that the existence of NBNCo is the only reason for this. In fact, I’d say that the iiBorg would have made a considerable number of acquisitions even without the NBN, simply because they could.

It’s just the way business works. Consolidation is everywhere, was going on long before the NBN and in fact has nothing to do with the NBN at all (apart from it being another business cost).

> 1) RSPs have to provide 1Gbps services from day one. They don’t, in fact most will probably slowly increase the maximum speed tier rather than offer 1Gbps.

> 2) In order for RSPs to provide 1Gbps service they must make it avaiable are every PoI. They don’t, they can pick and choose the most profitable areas to get 1Gbps first, thus reducing the impact.

By inference this means that on the NBN, only certain profitable locations will have access the faster speeds because it will uneconomic to provide 1Gbps services at many POIs. Is this better or worse than distance from the exchange with ADSL? Potentially RSPs could drop higher speeds from their plans if the economics don’t work out.

> 3) The cost of CVC is set at $20/Mbit. It’s not, the price, according the business plan, and basic common sense, is set to drop over time.

When average data usage reaches 570GB/month, CVC will drop as low as $8. Currently average data usage is under 20GB/month. At $10, it is still $1.936 million/month for a national network.

> What about their network configuration prevents this set-up? You can’t just say it, and expect us to believe you. Based upon your track record, including the easily demonstrable counter points I presented above, I don’t trust you to actually understand anything about the NBNCo pricing model and how it afters RSPs.

The fact that the cost of CVC means that POIs represent the chock point on the network. RSPs are unable to provide QoS on packets inside the NBN network that have the same class and higher classes of traffic cost more (5Mbps of class 1 is $330/month).

Given the implications I’ve pointed out of your points above, I suspect you may not have thought through the implications of what you are saying. Let me rephrase it for you: “NBNCo’s high charges for CVC mean that in many POIs RSPs will not be able to attract sufficient customers to make offering high speed plans viable.” if you want faster than HFC then you have better choose your POI very carefully.

> I don’t know if you know this but Flatrate plans were suggested by Exetel under the NBN after-all. Whether or not this was just a positing of a “better way to do thing” or something that Linton actually plans to implement remains to be seen, but there was no press release as far as I’m aware of saying “NBNCo’s pricing model stops us from offering this product, sorry.”

As explained above the lack of control that an RSP has over network traffic on the NBN means that technically it is difficult to prioritise packets except through brutal methods. Prioritisation of individual connection packets is a core part of Flatrate as implemented by Internode.

> Honestly, although consolidation by companies like the iiBorg occurs in part by NBNCo, you cannot assume that the existence of NBNCo is the only reason for this. In fact, I’d say that the iiBorg would have made a considerable number of acquisitions even without the NBN, simply because they could. Correlation does not imply causation Mathew.

True, acquisitions would have occurred. What I have shown is that CVC results in a minimum size that a national RSP needs to obtain to be financially viable has risen significantly compared with Telstra Wholesale (not that I support that model) and this is without considering the cost of backhaul from regional locations. Secondly what we have is a blog post from 2010, outlining the consequences of 121 POIs. Together these two facts suggest NBNCo is a driving force behind the consolidation and other commentators have

In short, yes, more profitable, read, more demand for 1Gbps services, areas will have 1Gbps enabled. However, you seem to have missed a key point from the plan on page 64.

What this little tibid means is that, unlike you who believe that 1Gbps or higher is the end game and by god if we don’t get 1Gbps we’re all going to die in the horrible fires of hell, NBNCo are being more conservative and realistic, and if they are proven wrong they will respond accordingly.

You might want to read up on the plan in a a little more detail. Particularly the following on page 67:

If it costs them that much they have at least 30,000 customers per CSA, meaning 3.63 million customers. A provider with this many customers will hold a considerable stack of the market.

With 3.63 million customers, that is $0.54/m in CVC per customer to offer the minimum required to deliver 1Gbps connections to all PoIs (i.e. 2Gbps). Effectively you’re quoting the best case, in terms of customers, with the worst case, in terms of demand.

The worst case is actually $1.791 million. That would be the minimum capital you would have to put forward if you wanted to offer 1Gbps to every PoI, as I stated before. Is it unreasonable to expect a critical mass of customers on a CSA before you start offering faster and faster services? I don’t think so.

And if an ISP does want to offer 1GBps from day one remember something Mathew, before building their network Google engaged the public and asked “How many of you would sign up if we offered X?” What stops an ISP from doing that here? Nothing.

The fact that the cost of CVC means that POIs represent the chock point on the network. RSPs are unable to provide QoS on packets inside the NBN network that have the same class and higher classes of traffic cost more (5Mbps of class 1 is $330/month).

Bullshit. I don’t actually think you know how QoS works. Let me explain:

RSPs effectively have a shared pipe (CVC) to all their customers. This pipe is 150Mbps + $X/Mbit for CSAs under 30,000 customers and $X/Mbit for CSAs over 30,000 customers. Within that network, a customer can only utilise a certain amount that as his or her “peak” bandwidth, their AVC. Within that pipe they can proritise certain packets over others.

Class traffic, on the other hand, applies only when the bandwidth available on a given link is less than the bandwidth of all of the CVC pipes in the network, in that case, Class 1 gets priority over Class 2, etc, etc. QoS implemented BY an RSP is merely a subclass, e.g. Class4A gets higher priority can Class4B).

Yes, we got that, you think this is a dealbreaker, and yet, no one here agrees with you, despite having access to all the resources you have, and even having the same, or possibly in some cases, even more so, insatiable appetite for bandwidth than you do.

As I said before, in the corporate plan, NBNCo are predicting a certain amount of demand, you’re predicting more, but NBNCo have explicitly said “if our predictions prove too conservative, we will respond accordingly, i.e. drop CVC and AVC prices”.

What part of this do you not understand? There is even scope in there to increase the free amount of CVC given to RSPs under the critical mass of customers in a CSA, provided, and here’s the kicker they can maintain enough revenue to pay for the network

In other words Mathew, if everyone actually wants 1Gbps services, NBNCo will find a way to deliver them. They’re, however, predicting, and I tend to agree with them, that most people won’t. Personally, since you give so much weight to your own personal opinion, I’ll give you mine: I think they got the 12Mbps only customers hilariously wrong, but I think 5% demand for 1Gbps in 2028 is reasonable.

What you have shown is that CVC results in a minimum size that a national RSP needs to option to be financially viable has risen significantly if the ISP intends to offer 1Gbps services. What you have not shown is how significant the rise is for RSPs who intend to offer the more common 12-100Mbps plans offered by every RSP currently on the NBN, and if 121 PoI is still the most significant factor in this area of the market.

Simon’s blog ALSO offered solutions to the problems the 121 PoIs present, one of them was to offer some starting CVC to decrease the burden, which NBNCo has done. Something you seem to neglect to mention.

Once again, correlation does not imply causation here. Show me causation?

I apologise, I misread a bit in the middle with free CVC, I wrote it before pulling out the specific quote from the Business Plan.

It says construction passes, not customers active. With that in mind, I will revise my statement below that to just:

Is it unreasonable to expect a critical mass of customers on a CSA before you start offering faster and faster services? I don’t think so. And if an ISP does want to offer 1GBps from day one remember something Mathew, before building their network Google engaged the public and asked “How many of you would sign up if we offered X?” What stops an ISP from doing that here? Nothing.

The Coperate plan showsprices will fall as demand rises and the fall in prices is significantly slower than the rise in demand.

I can only assume you’re referring to 8-9 on page 67. What you fail to release is that NBNCo are assuming businesses will utilise significantly more bandwidth than residential customers and will consequently pay more for it. If you take this assumption into account the price in the residential space should not be significantly affected.

Please don’t look at presented data out of context, it undermines your arguments significantly. As stated if their model proves incorrect they will respond.

Labor Ministers provided NBNCo with a Statement of Expectations. Labor Ministers review each Corporate Plan before it is published and given the length of time it is reasonable to assume request changes.

While true, how does this refute my statement? Are you saying there are applications that require 1Gbps that the ministers are simply not aware that will affect the majority of Australians? I follow technology quite closely and have no idea to what you refer.

It depends on you definition of affordable. The fact that 50% are predicted in the Corporate Plan suggests that it is not reasonably affordable.

Have you even looked at the actual, real world, demand and pricing? The corporate plans predictions are not set in stone, and once again, if they are wrong they will revise their predictions.

When you consider where the costs are it is a perfectly reasonable request. Network access in the Australian market is limited by quotas (excluding the few limited exceptions of congested ‘unlimited’ plans). As with other public utilities (water, power, gas) low access charges and usage based pricing is perfectly reasonable.

I don’t think you understand the true consequences of giving everyone a 1Gbps plan with limited quota. You would suddenly and dramatically increase backhaul demand well beyond what is capable of being provided.

This isn’t like water or electricity where even if we increase the input capacity of your line or pipe, your consumption rate is still limited. If you give someone a 1Gbps connection, they will use as much as they can. There isn’t a limit in the form of a tap or finite energy consumption.

They may only use it for fractions of a second at a time, but they are still using as much as they can.

The cost to NBNCo of providing a 12Mbps or 1Gbps service is close to zero. It does cost more to NBNCo to provide 2Gbps CVC versus 200Mbps, but it is not 10 times. You may have lost sight of the fact that the NBNCo wholesale charges are simply a financial model and that if you change the parameters, the wholesale charges change. For example Simon Hackett provided a slightly more expensive model that had a minimum speed of 100Mbps.

I acknowledge this about where I have said they can revise their plan if their predictions prove false, but you still fail to release that if they don’t introduce artificial scarcity, someone else will by virtue of our back haul needing continuous and unrelenting upgrades.

The Labor plan predicts that 50% on fibre will have 12Mbps. That 50% will almost certainly be the poor, who could benefit most. This will create a greater social divide than the Coalition plan.

See my responses above. Further how you think that the Coalition plan won’t create a similar cost disparity between plans despite having similar CAPEX requirements is beyond me. Magic I presume? Afterall according to you they offer free access to those who pay for FTTHoD.

Now we are getting down to the harsh reality:

* Unlikely all RSPs will offer 1Gbps services

* 1Gbps services are unlikely to be available from all POIs for commercial reasons.

> As I said before, in the corporate plan, NBNCo are predicting a certain amount of demand, you’re predicting more

It isn’t about demand. It is about the divergence between the promotion of 1Gbps and the reality that it will be expensive and that very few will have it. It is the divergence between the promotion of how the NBN will be used and the reality that Labor are content for 50% on fibre to connect at 12Mbps meaning they won’t be able to access those services.

My argument is that if we are building a national network, then it should be for the good of the people. I think Labor’s proposal falls far short of this, primarily because of the speed restrictions. While technically inferior, the Coalition plan has a higher minimum speed (50Mbps in 2019) than Labor’s plan and fibre is available for those who demand it.

> Simon’s blog ALSO offered solutions to the problems the 121 PoIs present, one of them was to offer some starting CVC to decrease the burden, which NBNCo has done. Something you seem to neglect to mention.

NBNCo should have been able to work this out, and I did mention NBNCo’s response elsewhere on this thread.

Which is only a problem for people who want 1Gbps services and if there are not other tangiable advantages to the technology other than the ability to do 1Gbps services over the alternatives.

Which is a minority, and there are. So you’re arguement falls short here.

It is the divergence between the promotion of how the NBN will be used and the reality that Labor are content for 50% on fibre to connect at 12Mbps meaning they won’t be able to access those services.

First of all, as was pointed out many times it isn’t Labor’s decision, it’s commerical decision by NBNCo based upon predicted demand. If they are wrong, they will revise prices accordingly as was pointed out above.

Secondly, all of the things promoted on the NBN do not actually require 1Gbps, but a considerable amount of them may require more than 25Mbps. Under the Coalition plan you are only assured to get 25Mbps, with a possible upgrade to 50Mbps, and you might get more depending on your circumstances. This is opposed to 100Mbps being reasonably affordable and widely avaliable under the NBN. So it is not mispromoting the NBN, they have only said “Up to 1Gbps services avaiable”, which they are. It didn’t say anything about them being affordable, or essitential. In fact, the majority of press associated with the NBN assume that people will be, for the short and medium term, able to do everything they need to under 100Mbps.

You arguement is sound, a network of this scale should be for the good of the people. Your drawn conclusions are not, because they rely on a false premise because you seem to be equating “for the good of the people” with “giving everyone 1Gbps services”, which is not reasonable, and only something a pure Technocrat would consider, taking technical capabity over economic practicility.

Effectively you’re asking Labor to commit to providing the NBN out of the government coffers, and then allowing the Coalition to provide a plan that will pay for itself, rather then acknowleding the releative differences between the two plans and asking yourself is the extra amount NBNCo commits to CAPEX worth it in the long term, which, due to upgradiblity, I would agrue most definately.

You are being unreasonable if you assume that just because Simon Hackett put forward compelling and helpful arguements to explain a problems that 121 PoIs present that this consequences would immediately be obvious to NBNCo.

> First of all, as was pointed out many times it isn’t Labor’s decision, it’s commerical decision by NBNCo based upon predicted demand. If they are wrong, they will revise prices accordingly as was pointed out above.

The Corporate Plan shows how prices will fall as demand rises and the fall in prices is significantly slower than the rise in demand.

> Secondly, all of the things promoted on the NBN do not actually require 1Gbps, but a considerable amount of them may require more than 25Mbps. Under the Coalition plan you are only assured to get 25Mbps, with a possible upgrade to 50Mbps, and you might get more depending on your circumstances.

Labor Ministers provided NBNCo with a Statement of Expectations. Labor Ministers review each Corporate Plan before it is published and given the length of time it is reasonable to assume request changes.

> This is opposed to 100Mbps being reasonably affordable and widely avaliable under the NBN. So it is not mispromoting the NBN, they have only said “Up to 1Gbps services avaiable”, which they are. It didn’t say anything about them being affordable, or essitential. In fact, the majority of press associated with the NBN assume that people will be, for the short and medium term, able to do everything they need to under 100Mbps.

It depends on you definition of affordable. The fact that 50% are predicted in the Corporate Plan suggests that it is not reasonably affordable.

> You arguement is sound, a network of this scale should be for the good of the people. Your drawn conclusions are not, because they rely on a false premise because you seem to be equating “for the good of the people” with “giving everyone 1Gbps services”, which is not reasonable, and only something a pure Technocrat would consider, taking technical capabity over economic practicility.

>

> When you consider where the costs are it is a perfectly reasonable request. Network access in the Australian market is limited by quotas (excluding the few limited exceptions of congested ‘unlimited’ plans). As with other public utilities (water, power, gas) low access charges and usage based pricing is perfectly reasonable.

The cost to NBNCo of providing a 12Mbps or 1Gbps service is close to zero. It does cost more to NBNCo to provide 2Gbps CVC versus 200Mbps, but it is not 10 times. You may have lost sight of the fact that the NBNCo wholesale charges are simply a financial model and that if you change the parameters, the wholesale charges change. For example Simon Hackett provided a slightly more expensive model that had a minimum speed of 100Mbps.

> Effectively you’re asking Labor to commit to providing the NBN out of the government coffers, and then allowing the Coalition to provide a plan that will pay for itself, rather then acknowleding the releative differences between the two plans and asking yourself is the extra amount NBNCo commits to CAPEX worth it in the long term, which, due to upgradiblity, I would agrue most definately.

The Labor plan predicts that 50% on fibre will have 12Mbps. That 50% will almost certainly be the poor, who could benefit most. This will create a greater social divide than the Coalition plan.

“While technically inferior, the Coalition plan has a higher minimum speed (50Mbps in 2019) than Labor’s plan and fibre is available for those who demand it.”

Where did you get the crazy idea that the Coalition plan is “One speed for all”? The 25 and 50Mbps numbers are the maximums, not the “base” plan…

@Tinman_au

> Where did you get the crazy idea that the Coalition plan is “One speed for all”? The 25 and 50Mbps numbers are the maximums, not the “base” plan…

Quoting from Faste. Affordable. Sooner. The Coalition’s plan for a better NBN: “Download speeds of between 25 and 100 megabits per second by the end of 2016 and 50 to 100 megabits per second by 2019.”

Clearly the 25 & 50Mbps are the minimum speeds.

The Coalition also are correctly focusing on areas of greatest need first. Compare that with Labor where they are overbuilding cable areas first.

> Telstra’s wholesale was a very different scenario. Telstra Wholesale delivered the data to capital cities, whereas NBNCo is 121

You’ve already been paying for back-haul to various exchanges for naked DSL. Your arguing with NBN it costs ‘alittle more’ suggest we should all go camping and sing happy stories together?

It doesn’t make alot of sense

Using a theoretical scenario/situation to explain this:

A successful ISP/Telecommunication provider.

It would be quite cleaver of ISP/Telecommunication provider manufacture media release. Which painting a dark future with the NBN that could scare off new competition, Meanwhile you this company could manufactured excuse for own monopoly

Also dividing attention away a company XDSL investment that gets obviously undermined by the NBN rollout. Meaning if you running at a loss under the NBN

It would be in the best companies interest to prevent any competition. To recover they’re own investments

Having said that. Nothing stopping someone from setting up a State based ISP and being quite successful then eventually going natural once establishing themselves

Its been done before under the same conditions of what we have now with the NBN

> You’ve already been paying for back-haul to various exchanges for naked DSL. Your arguing with NBN it costs ‘alittle more’ suggest we should all go camping and sing happy stories together?

CVC charges levied by NBNCo are significantly more than backhaul services. The backhaul to various exchanges is equivalent to the backhaul required from each POI to separate network points.

> Using a theoretical scenario/situation to explain this:

Clearly you have no understanding as to the character of Simon Hackett and Internode. I suggest you spend some time reading his commentary and realise that Internode was built on doing the right thing by customers.

I suggest you might want to read these blog posts for some more background on the effect of 121 POIs on competition. In particular pay attention to the “NBN Retail Pricing Pressure Points” and Simon’s proposal that NBNCo offer 200Mbps of CVC free per POI. You may wish to consider why NBNCo made several months later to provide 150Mbps of CVC free.

Seriously Mathew, so, apparently NBNCo has to be perfect, can’t listen to their customers when they get something wrong?

They have to get it right first time. My god, you’re more arrogant than I thought. Let me guess, you’re going to rip me apart for misremembering a quote in the corporate plan in my above post because I wasn’t perfect first time.

If that’s your attitude, I really don’t want to both with this argument further.

I suggest you might want to read these blog posts for some more background on the effect of 121 POIs on competition.

Perhaps you should start canvassing the Liberals about it Mat, they will also have 121 POI’s and be in a position to do something about it (after Sept 14 apparently)…

> Perhaps you should start canvassing the Liberals about it Mat, they will also have 121 POI’s and be in a position to do something about it (after Sept 14 apparently)…

You are right it probably is pointless to discuss Labor’s NBN plans, because in 6 years they have vastly over promised and delivered very little. Based on the maps for stage 2 published prior to the last Federal Election, I should have had my 1Gbps connection for a couple of years by now. Currently the NBNCo rollout map suggests March 2018.

Will be good to see Annex M on residential plans for iiNet users :)

Comments are closed.